.svg)

📌 Key Takeaways

- Filing a mechanic's lien preserves your right to pursue payment but does not compel payment — enforcement through a foreclosure lawsuit is required.

- Every state sets an enforcement deadline, ranging from 90 days to two years, within which a subcontractor must file suit or the lien lapses.

- Missing the enforcement deadline eliminates the security interest in the property, leaving subcontractors to pursue debt through civil court without leverage.

- Before the enforcement deadline, subcontractors can negotiate payment, extend the lien by agreement, or file a lawsuit to foreclose on the property.

You recorded the lien. The property owner got notice. And now...nothing. No check, no call, no resolution. So, what did filing the mechanic's lien actually accomplish? And what are you supposed to do next?

This is where many subcontractors get stuck. Filing a lien preserves your right to pursue payment, but it doesn’t compel it. There is a second step—enforcement—and every state gives you a specific window to take it. Miss that window, all the leverage you earned ceases and you're left chasing the debt through civil court without any security interest in the property.

So, what to do? This article walks you through what happens the moment a mechanic's lien is recorded, what the enforcement process actually looks like, and how to make sure you don't lose your rights on a technicality.

What happens when a mechanic's lien is recorded?

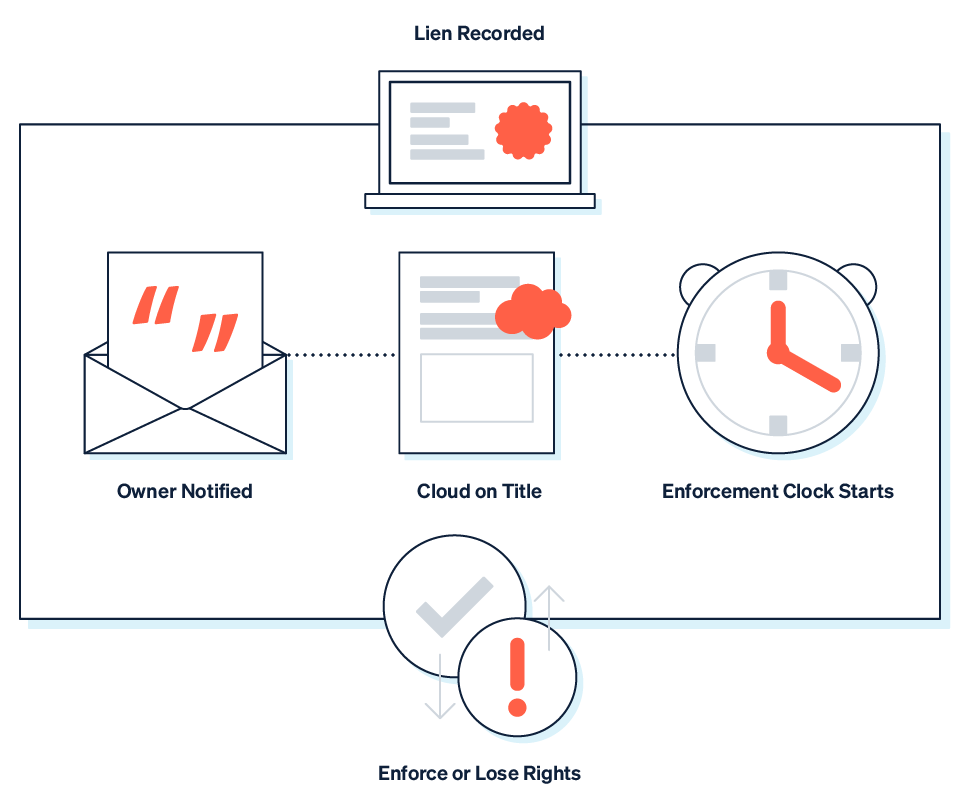

The second a lien is recorded in the county recorder's or clerk's office, three things happen simultaneously.

- The property owner receives notice, either through service requirements built into state law or through the public record itself. They now know there's a claim against their property.

- The lien attaches to the property's title as a "cloud,” which is a legal encumbrance that makes the property significantly harder to sell or refinance. Lenders won't close a loan on a property with an active mechanic's lien, and title companies won't issue clean title insurance. That's your leverage.

- A state-specific enforcement clock starts ticking.

That last point is the one that matters most for what comes next.

What’s the difference between filing a lien and enforcing a lien?

Filing a mechanic's lien and enforcing a mechanic's lien are two separate legal acts. Most subcontractors know how to file one. Far fewer know that filing alone isn’t actually what gets them paid.

Filing the lien gives you a legal claim against the property and puts the world on notice. Enforcing the lien—which you do by filing a lawsuit to foreclose on that claim—is what forces the issue. A foreclosure action asks the court to order the property sold to satisfy the debt, which is why property owners take it seriously.

Oftentimes, the threat of enforcement is often enough to trigger payment. Many disputes are resolved through negotiation once the owner sees a foreclosure complaint. But you need to be prepared to follow through, because the clock doesn't care whether you're in negotiations or not.

How long does a mechanic's lien last before it expires?

A mechanic's lien does not last forever. Every state sets an enforcement deadline—sometimes called the "suit to foreclose" deadline—within which you must file a foreclosure lawsuit or the lien lapses. These deadlines vary significantly by state, ranging from 90 days to two years.

Here’s a quick reference for several major construction states:

These are general guidelines, and state lien laws change. Always verify the deadline in the specific state where the project is located before assuming you know the window. See Siteline's state-by-state lien rights guides for precise requirements by jurisdiction.

What does the enforcement process look like?

If the owner hasn't paid, and you're approaching the enforcement deadline, here’s what the mechanic’s lien foreclosure process typically involves. It's not quick, and it's not free, but it's the path that’ll get you paid.

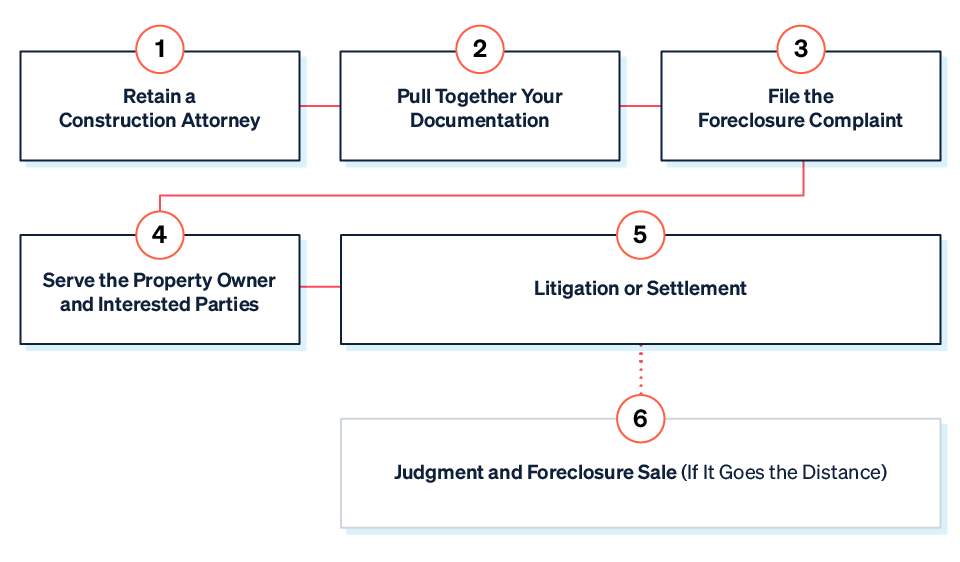

1. Retain a construction attorney.

Some states require that a licensed attorney file the foreclosure complaint. Even where it isn't required, this is not a process to navigate alone. A construction attorney who knows your state's lien law will protect you from procedural errors that could tank an otherwise valid claim. Engage one early, ideally before the enforcement window gets tight.

2. Pull together your documentation.

Before filing, you need to assemble a complete paper trail:

- The original contract

- All change orders

- Every pay application submitted

- The payment history (including what was paid and when)

- Correspondence about the disputed balance

- The recorded lien itself

This documentation is the foundation of your foreclosure complaint. Gaps here give the other side room to poke holes in your argument.

3. File the foreclosure complaint.

File the foreclosure lawsuit in the county where the property is located, not where your company or the client’s company is based. The complaint asks the court to enforce your lien claim and to order the property sold to satisfy the debt if no other resolution is reached. Your attorney will prepare and file this with the appropriate court.

4. Serve the property owner and interested parties.

The property owner—along with any other parties with a legal interest in the property (like the lender, whose mortgage sits alongside your lien, and the general contractor)—must be served with the complaint. State law specifies acceptable methods of service. Serving the wrong parties, or serving them incorrectly, can set the whole case back.

5. Enter litigation or settlement.

This is where most cases end. Once the owner sees an actual foreclosure complaint filed in court, the calculation shifts for everyone involved—lenders grow nervous, the title becomes complicated, and buyers walk away. As the pressure escalates, many disputes settle through negotiation, whether via lump-sum payment, a payment plan, or a reduced settlement in exchange for lien release.

Settlement here is not a sign of weakness. It's often the fastest path to payment, and the foreclosure filing is what created the urgency to get there.

6. Proceed to judgment and foreclosure sale (if it goes the distance).

If the case doesn't settle, the court will eventually issue a judgment. If the judgment favors the lienholder, the court can order the property sold at a foreclosure sale to satisfy the debt. In practice, this outcome is rare—most disputes resolve well before it reaches this point—but the possibility of it is what makes the mechanic's lien a serious collection tool. The threat is credible because the consequence is real.

What happens if you miss the enforcement deadline?

The lien expires, the cloud on the title evaporates, and the leverage you had—the thing that was making refinancing impossible and title insurance unavailable—disappears.

You still have a contract claim. You can still sue for the unpaid balance. But you're now doing that through ordinary civil litigation, without a security interest in the property and without the urgency that comes from a title cloud. That is a meaningfully weaker position, and in many cases, the practical leverage to compel payment is gone.

Missing the enforcement deadline is one of the most common—and most preventable—ways subcontractors lose valid payment claims. The lien filing process gets attention; the enforcement window often does not. (For more on the mistakes that can void or weaken lien rights, see What Voids a Mechanic's Lien—and Other Mistakes That Can Kill Your Rights.)

How do you keep track of your lien enforcement deadline?

Here's the practical problem: lien deadlines are project-specific. On any given day, a subcontractor might have active liens on projects in three different states, each with a different enforcement window, recorded on different dates. Tracking all of this manually—in a spreadsheet or a calendar reminder someone set up six months ago—is how you miss deadlines.

The enforcement deadline needs to be tracked the same way as the original filing deadline: automatically, from the date of recording, and with a clear alert before it expires.

That's what Siteline's Lien Rights Tracker does. It tracks both the original filing deadline and the enforcement deadline for every project, and flags them before either one slips. Subs working across multiple states—where the windows range from 90 days to two years—can't afford to rely on someone's memory for this. The dollar amounts are too large, and the consequences of a missed deadline are too permanent.

Frequently Asked Questions

What happens when a mechanic's lien is filed?

When a mechanic's lien is filed, it attaches to the property's title as a legal encumbrance, making the property difficult to sell or refinance until the lien is resolved. The property owner receives notice of the claim, and a state-specific enforcement clock starts. Filing alone does not compel payment; it merely preserves the claimant's right to pursue payment through a foreclosure lawsuit.

Does a mechanic's lien expire if I don't enforce it?

Yes. Every state sets an enforcement deadline—the window in which the lienholder must file a foreclosure lawsuit or the lien lapses. These deadlines range from 90 days (California) to two years (Texas, for commercial projects). Once the window closes, the lien expires, and the property owner can have the cloud on the title removed. The claimant loses the security interest in the property.

How long do I have to enforce a mechanic's lien?

The enforcement window varies by state. Common examples: California gives 90 days; Arizona and Colorado give six months; Florida and New York give one year; and Texas gives up to two years, depending on the project type. The window runs from the date the lien was recorded, not the date work was completed. Check the specific requirements for the state where the project is located.

Can a mechanic's lien force foreclosure on a property?

Yes. Enforcing a mechanic's lien means filing a foreclosure lawsuit and asking the court to order the property sold to satisfy the unpaid debt. In practice, most disputes settle before a foreclosure sale occurs, because property owners, lenders, and title companies are strongly motivated to resolve a lien before it reaches that point. The foreclosure mechanism is what gives the lien its leverage.

What is the difference between filing and enforcing a mechanic's lien?

Filing a mechanic's lien records the claim in the public record, creates a cloud on the property's title, and starts the enforcement clock. Enforcing a mechanic's lien means filing a foreclosure lawsuit within the state's deadline to compel payment or force a property sale. While filing is the first step, enforcement is what actually produces payment.

What happens if I miss the mechanic's lien enforcement deadline?

The lien expires, the cloud on the title ceases, and the claimant loses the security interest in the property. The unpaid debt still exists, and you can pursue it through ordinary civil litigation, but without the lien, you as the claimant have no priority claim against the property. Missing the enforcement deadline is one of the most common ways subcontractors lose valid payment claims.

Do I need an attorney to enforce a mechanic's lien?

Some states require a licensed attorney to file the foreclosure complaint. Even where it's not required, working with a construction attorney is strongly recommended. Procedural errors—improper service, incorrect court, missing documentation—can invalidate a lien foreclosure action. Given the dollar amounts typically at stake, legal guidance is worth the cost.

AIA®, G702®, and G703® are registered trademarks owned by The American Institute of Architects and ACD Operations, LLC. Siteline is not affiliated with The American Institute of Architects or ACD Operations, LLC. Users who wish to use Siteline’s software to assist in filling out AIA® forms must have or secure the AIA® forms. Siteline does not and will not provide users with the forms.

%202.webp)